For many years, federal tax credits have helped businesses make the switch to solar by significantly reducing the upfront cost of installing a solar system.

Those incentives are still available for commercial solar projects, but the rules have recently changed. New legislation has introduced firm deadlines and additional requirements that businesses must meet in order to qualify for the full federal tax credit.

The opportunity is still very real. Businesses that move forward with solar in the near term can still take advantage of the 30% federal tax credit while lowering their long-term operating costs.

What has changed is the timeline. Companies interested in claiming these incentives now need to plan ahead and ensure their projects meet specific deadlines for construction and sourcing requirements.

In this article, we’ll walk through what these new rules mean for commercial building owners and how businesses can still successfully claim the federal solar tax credit.

Quick Summary

- The long-term timeline for commercial solar tax credits has been replaced with new deadlines of July 4, 2026 and December 31, 2027.

- Businesses must follow new “beginning of construction” rules and equipment sourcing requirements to qualify for the full 30% federal tax credit.

- Exact Solar has already secured 36 pre-certified project slots that allow qualified businesses to move forward with confidence under earlier rules.

- If your business is considering solar, it is important to begin evaluating your options within the next few months.

If you’d like to explore whether your building is a good candidate for solar, our team would be happy to walk through the details with you.

NOTE: This article is provided for general informational purposes only and should not be considered tax, accounting, or legal advice. Federal solar incentives are complex and subject to change, and eligibility depends on many project-specific factors. Businesses interested in claiming tax credits should always consult with a qualified tax professional before making financial or tax-related decisions.

Table of Contents

History of the Federal Commercial Solar Tax Credit

Federal incentives for solar energy have been around for decades. They are not new, and were not invented by the Biden Administration. They were actually first introduced in 1978 and later reestablished in 2005 by George W. Bush. Since then, these programs have helped thousands of businesses invest in solar by reducing the upfront cost of installing a system.

Most recently, the Inflation Reduction Act passed in 2022 expanded and extended these incentives, creating what many in the industry referred to as a stable long-term runway for solar investment.

That timeline changed in July 2025 when new federal legislation updated the structure of these incentives and introduced a faster phaseout schedule for solar tax credits.

Because of these changes, many business owners believe the solar tax credit has already expired. That is understandable, but it is not the case.

The residential solar tax credit ended on December 31, 2025, but the commercial solar tax credit is still available. What has changed is the timeline and the requirements businesses must meet in order to claim it.

Under the current rules, commercial solar projects can still qualify for the federal tax credit through December 31, 2027. However, projects must meet specific construction and sourcing requirements to remain eligible for the full incentive.

We’ll walk through what those requirements look like and how businesses can still take advantage of the federal solar tax credit before the program phases out

Commercial Solar Tax Credits Are Still Available for Businesses

Recent changes to federal policy have adjusted how businesses qualify for solar tax credits, but the incentives are still available for commercial projects.

Today, businesses can claim the federal Clean Electricity Investment Credit (Section 48E) for qualifying solar installations. In most cases, this credit covers 30% of the project cost.

What has changed is that projects must now meet two additional requirements:

- Construction timing rules, known as “Beginning of Construction” requirements

- Equipment sourcing standards that limit the use of components from certain foreign manufacturers

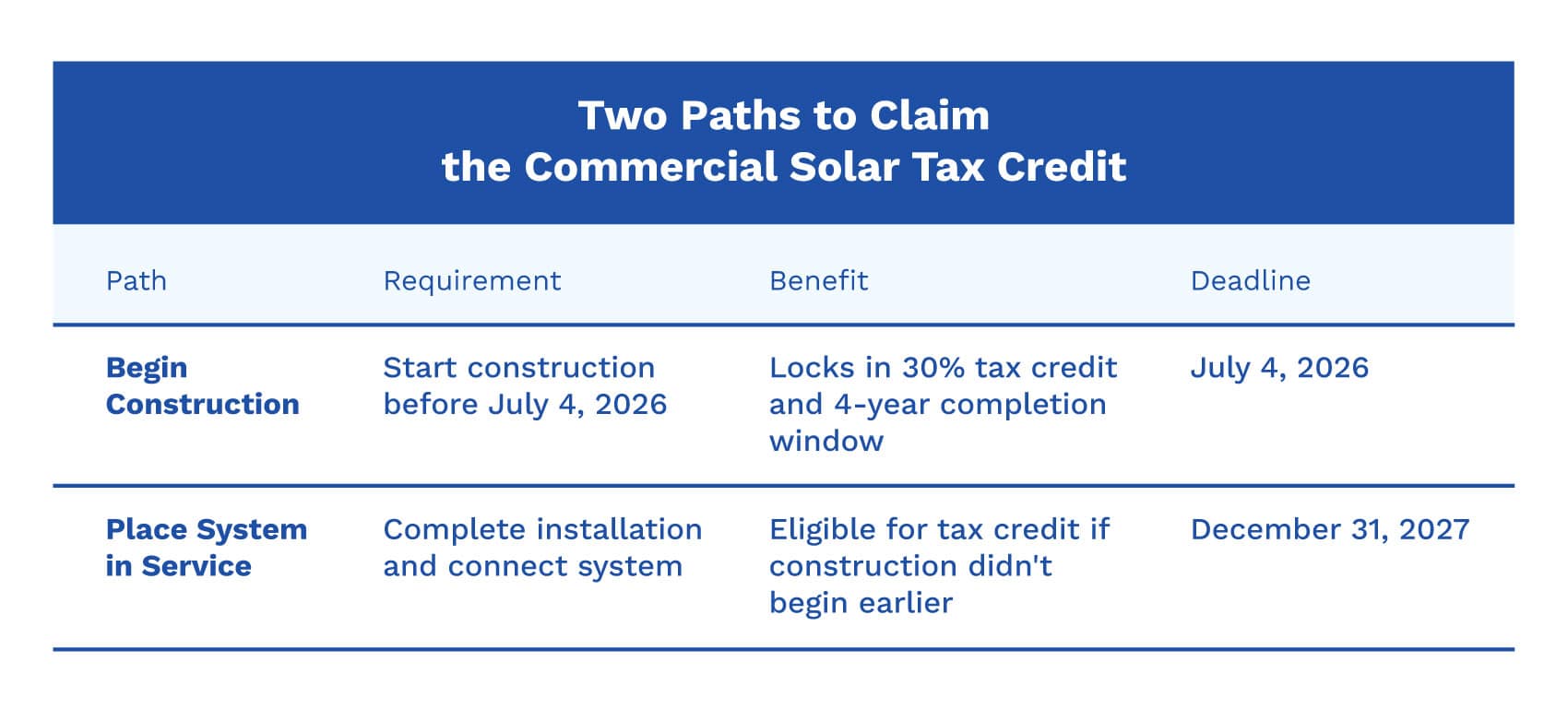

Businesses interested in claiming the full tax credit must now follow one of two paths.

Option 1: Begin Construction by July 4, 2026

If a project legally begins construction on or before July 4, 2026, the system can still qualify for the full 30% federal tax credit. Once construction begins, the project receives a four-year continuity window to complete the installation.

For most commercial solar systems, construction can be considered started by meeting one of the following IRS standards:

• 5% Cost Safe Harbor for projects 1.5 MW (AC) or smaller

• Physical Work Test for larger projects

Projects that successfully meet the beginning-of-construction requirement must then be placed in service by December 31, 2030.

Option 2: Complete the Project by December 31, 2027

If construction does not begin before the July 4, 2026 deadline, the remaining path to claim the tax credit is to fully complete the solar project and place it in service by December 31, 2027.

This means the system must be installed, interconnected with the utility, and producing electricity before that deadline.

Projects that miss this timeline will no longer qualify for the federal investment tax credit.

If you are considering solar for your business, starting the process early can help ensure your project meets the required deadlines. Our team would be happy to walk through the details and help determine whether your building is a good candidate.

How the IRS Determines Eligibility

Since the “One Big Beautiful Bill” (OBBB) passed in 2025, solar developers and installers across the country have been waiting for additional guidance from the IRS on how these new rules will be applied in practice. While the final regulations have not yet been released, the IRS and U.S. Treasury recently issued interim guidance that helps clarify how projects will be evaluated.

On February 12, 2026, the IRS released Notice 2026-15, which outlines how the government plans to measure whether a project relies too heavily on materials sourced from certain restricted manufacturers, referred to as Foreign Entities of Concern (FEOC).

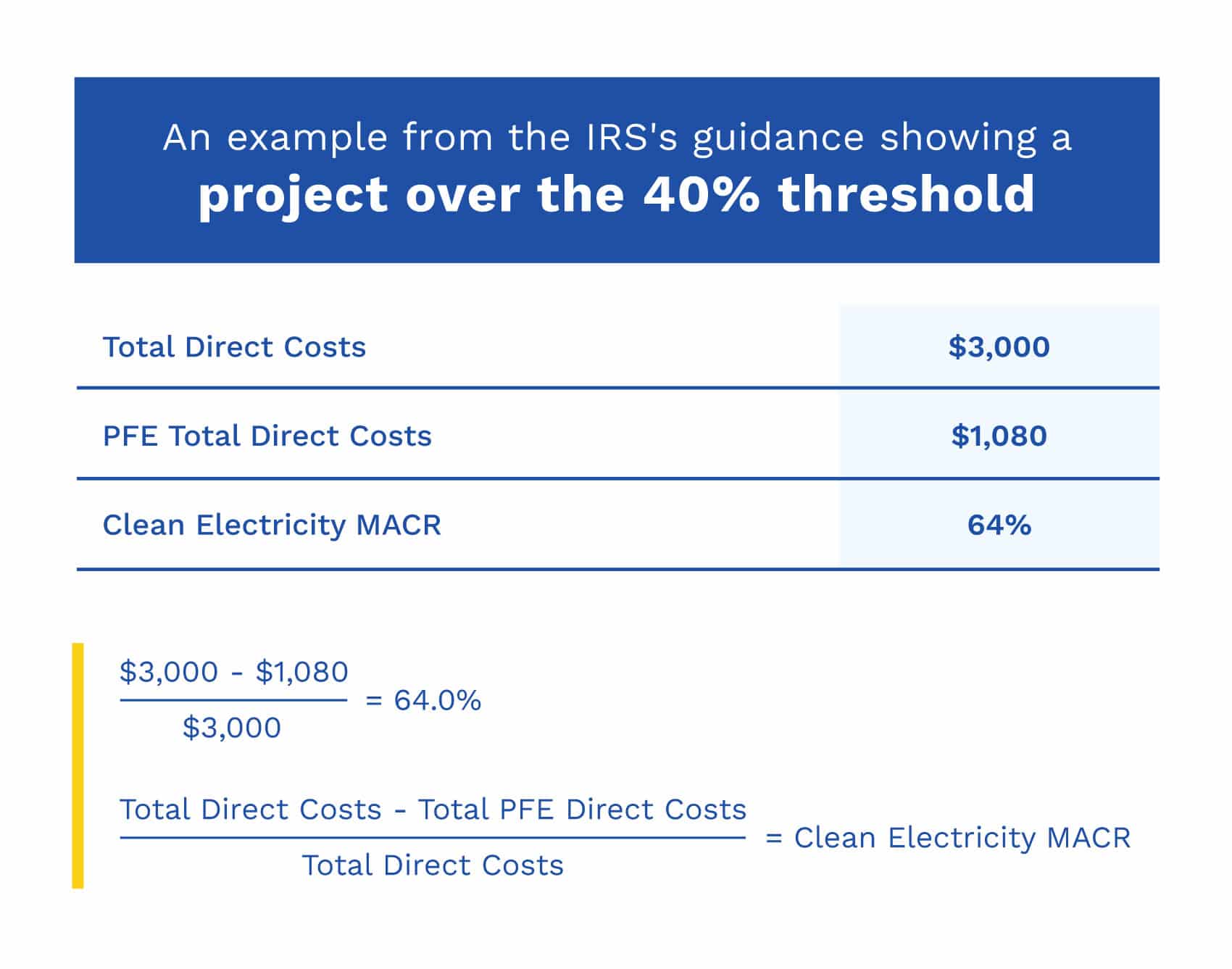

To determine compliance, the IRS introduced a calculation called the Material Assistance Cost Ratio (MACR).

This test measures the percentage of equipment in a solar project that comes from approved sources. For commercial solar projects that begin construction in 2026, the project must reach a MACR of at least 40% in order to qualify for the federal tax credit.

If a project falls below this threshold, it will not be eligible for the incentive.

The MACR Formula

The IRS measures FEOC compliance using a formula based on the direct cost of equipment used in the project.

MACR = (A − B) ÷ A

Where:

A = The total direct cost of all manufactured equipment used in the solar project

B = The direct cost of any equipment produced or supplied by a Prohibited Foreign Entity (PFE)

Safe Harbor for Equipment Tracking

Tracking the exact manufacturing cost of every component in a solar project would be extremely difficult for most developers. To simplify this process, the IRS allows projects to rely on safe harbor tables.

These tables assign standard values to certain solar components, such as:

• solar modules

• inverters

• racking systems

• electrical equipment

By using these safe harbor values, developers can calculate the MACR without needing proprietary cost data from manufacturers.

In practice, this allows solar installers like Exact Solar to structure projects in a way that meets the required thresholds while keeping the process manageable for building owners.

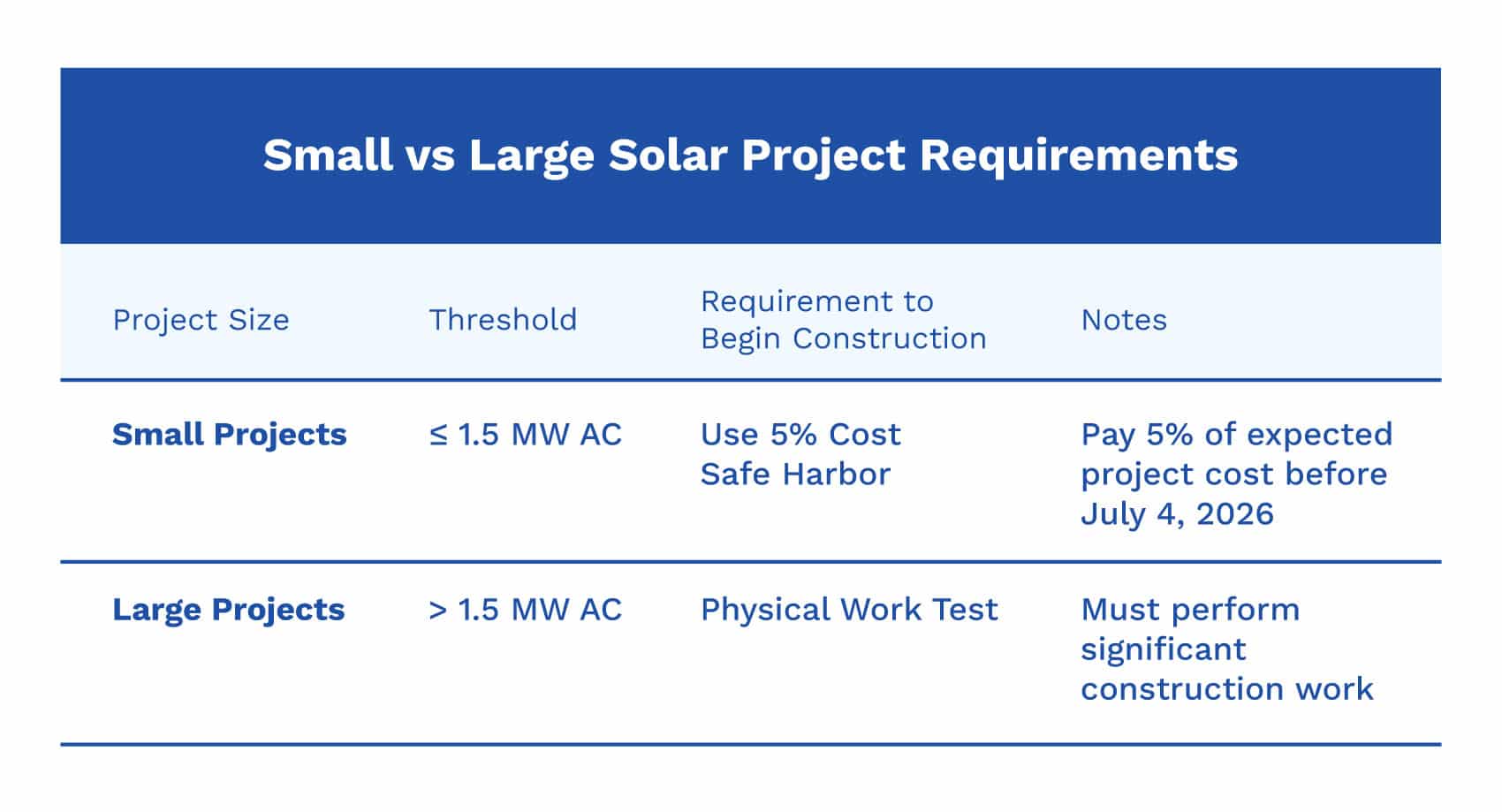

Exception for Small Projects (Less than 1.5 MW AC)

The IRS provides an important exception for smaller solar installations, making it easier for many commercial building owners to qualify for the tax credit.

Projects with a total capacity of 1.5 MW (AC) or less are classified as “Small Projects.” These systems are still allowed to use the 5% Cost Safe Harbor to establish that construction has begun.

For most commercial buildings, this threshold is quite large. The vast majority of commercial solar systems Exact Solar installs fall well below 1.5 MW.

How the 5% Cost Safe Harbor Works

Under this rule, construction is considered to have officially begun once the project owner has paid at least 5% of the total expected project cost before the required deadline.

In many cases, this requirement can be satisfied by placing a non-refundable deposit on major project equipment, such as solar modules or inverters that are being reserved for the project.

Meeting this requirement allows the project to lock in eligibility for the federal tax credit without needing to begin physical construction immediately. For smaller commercial projects, this provides a practical way to secure the incentive while final design, permitting, and scheduling move forward.

Large Project Requirements (More than 1.5 MW AC)

Solar projects larger than 1.5 MW (AC) follow a different path for establishing that construction has begun.

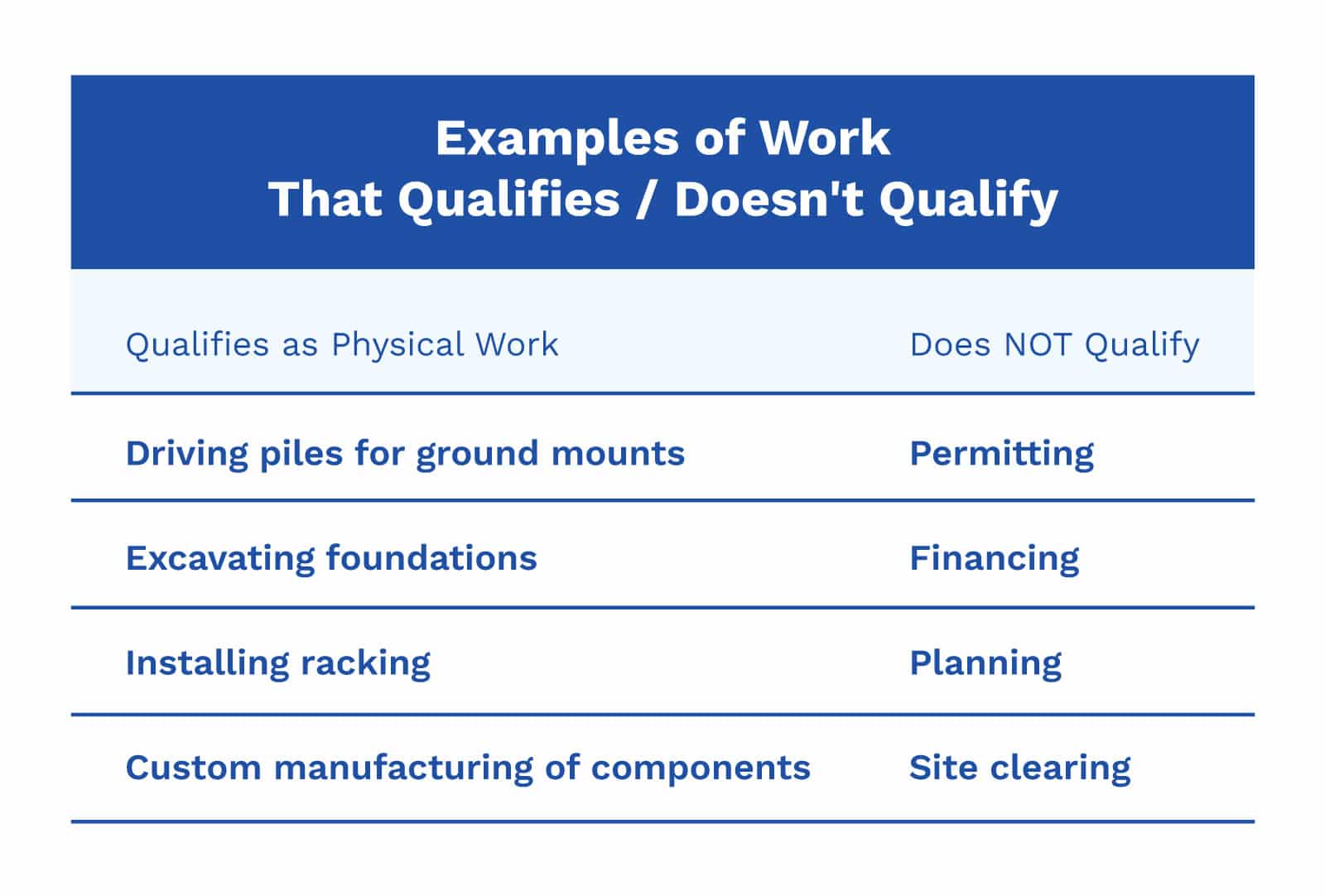

For these larger systems, the 5% Cost Safe Harbor is no longer available under the updated rules. Instead, projects must satisfy what the IRS calls the “Physical Work Test”, requiring “physical work of a significant nature” to begin before the deadline.

This means that meaningful construction activity must begin before the required deadline in order for the project to qualify for the tax credit.

Examples of qualifying work may include:

• installing foundations or piles for a ground-mounted system

• beginning racking installation

• excavation work related to project construction

• manufacturing custom electrical equipment or transformers specifically for the project

Certain early-stage activities do not count toward this requirement. Tasks such as permitting, financing, site planning, or basic site preparation are considered preliminary work and do not qualify as beginning construction under IRS guidance.

While these rules primarily apply to very large installations, they are important for companies developing utility-scale or large industrial solar projects.

For most commercial buildings, however, systems will fall below the 1.5 MW threshold, allowing them to use the simpler 5% Cost Safe Harbor described in the previous section.

The Advantage of Partnering With Exact Solar

Because the rules around federal solar incentives have been evolving quickly, Exact Solar took steps in 2025 to help protect future commercial projects for our clients.

After consulting with partners at the Amicus Solar Cooperative, we completed the steps necessary to establish 36 safe harbor project allocations before the December 31, 2025 deadline. By doing this, we were able to legally establish the “beginning of construction” status for these projects under the earlier rules. These allocations can now be assigned to future commercial projects.

For qualified businesses, this provides a clearer, more predictable path to claim the federal solar tax credit.

What This Means for Businesses

Commercial building owners who claim one of our 36 slots will benefit from three financial and operational advantages:

- They Freeze the Clock at 2025 Rules: These projects are grandfathered under the pre-OBBB regulations.

- Lock in a 4-Year Continuity Window: Projects using our pre-registered slots are granted a full 4-year safe harbor. This means you’ll have until December 31, 2029, to complete your installation.

- Guaranteed 30% Tax Credit: By using our established BOC, you eliminate the risk of missing critical deadlines and losing your federal funding.

These project allocations are limited and available for qualifying commercial and industrial solar installations on a first-come, first-served basis.

If your business is considering solar, our team would be happy to explain how this process works and whether one of these project slots may be a good fit.

How Businesses Claim the Commercial Solar Tax Credit

NOTE: Exact Solar is a solar design and installation company, not a tax, accounting, or legal advisor. The information below reflects our understanding of current federal guidance and typical project workflows, but it should not be interpreted as tax advice. Every business and project is different, and tax credit eligibility ultimately depends on the interpretation of federal law by the IRS and your tax professional. Business owners should always consult a qualified CPA or tax advisor before claiming any federal energy incentives.

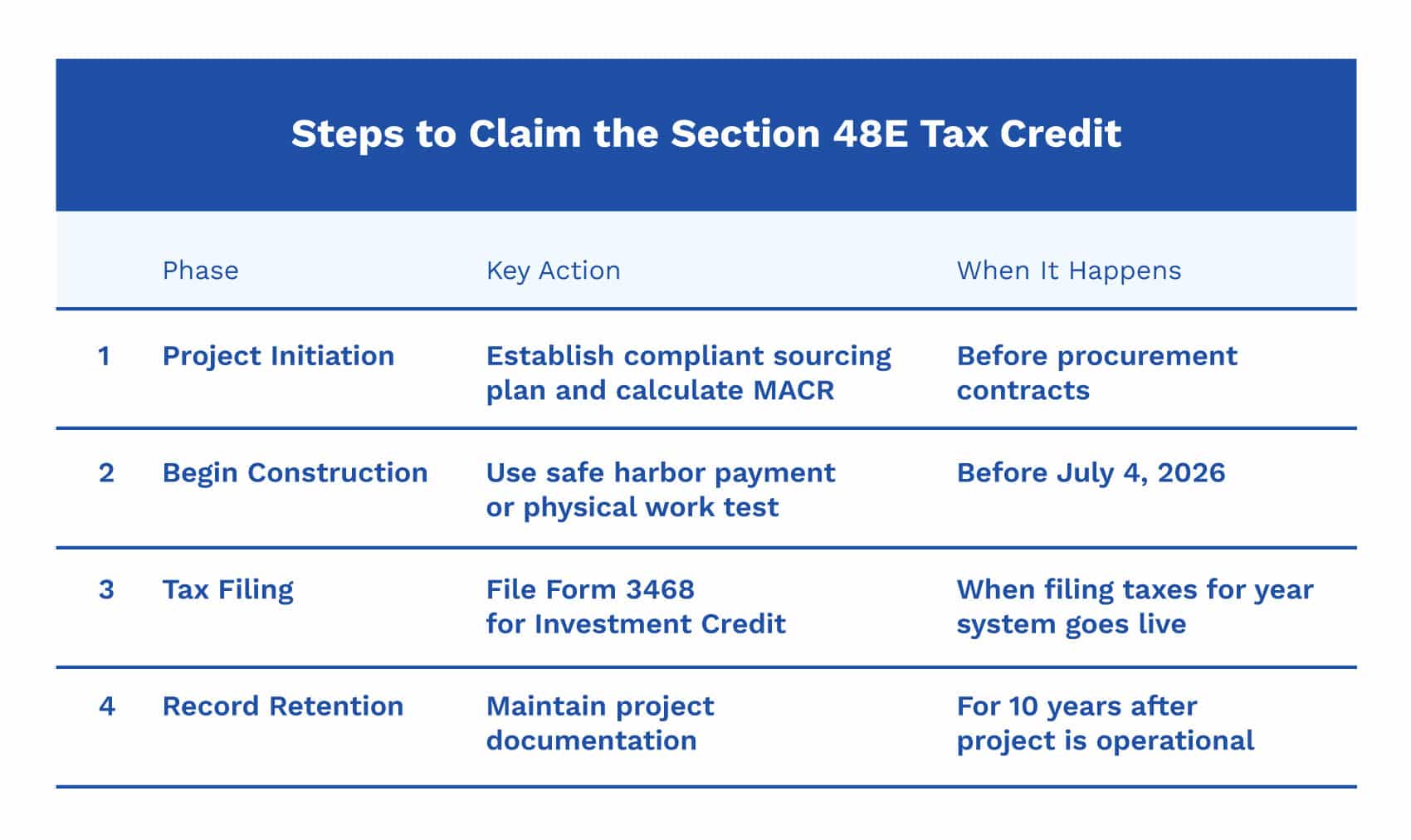

While every project is different, most commercial solar installations follow a process similar to the one outlined below when claiming the federal investment tax credit.

Phase 1: Project Initiation

This phase must occur before procurement contracts are signed.

Establish a Compliant Sourcing Plan

Projects must meet the required Material Assistance Cost Ratio (MACR) based on the year construction begins. The design must use components from a non-Prohibited Foreign Entity (PFE) that meet the minimum percentage requirement.

For projects beginning in 2026, at least 40% of system components must come from approved sources in order to qualify for the tax credit. This requirement increases to 45% for projects beginning in 2027.

If you partner with Exact Solar, our team will handle this for you. We will evaluate these sourcing requirements during the project design phase. For projects using one of our 36 pre-established safe harbor allocations, these sourcing requirements have already been taken care of.

Phase 2: Safe Harboring or Beginning Construction

Projects must establish that construction has officially begun before the applicable federal deadline.

For Projects Smaller than 1.5 MW (AC)

Most commercial solar systems fall into this category. These projects can meet the requirement using the 5% Cost Safe Harbor, which requires the project owner to pay at least 5% of the total expected project cost before the deadline.

In many cases, this payment is made as a non-refundable deposit on major equipment, such as solar modules or inverters reserved specifically for the project.

For Projects Larger than 1.5 MW AC

Larger projects must meet what the IRS calls the “Physical Work Test”, which requires meaningful construction activity to begin before the deadline.

Examples of qualifying work may include installing foundations, driving piles for ground-mounted systems, installing racking structures, or manufacturing custom electrical equipment for the project.

Preliminary steps such as permitting, planning, financing, or site clearing do not qualify as beginning construction under IRS guidance.

Phase 3: Tax Credit Filing

Once the solar system is installed, interconnected with the utility, and receives Permission to Operate (PTO), the project is considered placed in service.

The federal investment tax credit is typically claimed when the business files its tax return for that year.

In most cases, the credit is calculated and reported using IRS Form 3468 (Investment Credit) (Part IV, Section B).

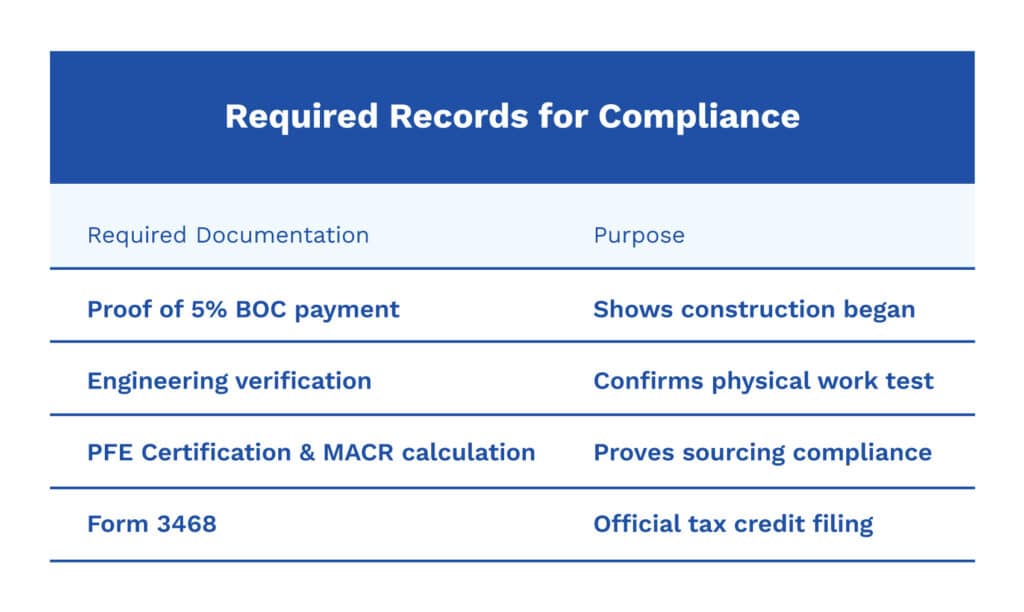

Phase 4: Record Retention

Businesses should maintain project documentation for at least ten years after the system is placed in service.

During this time, a complete digital record of the project should be retained to support any potential IRS review. This documentation should include:

• proof of the 5% safe harbor payment

• documentation supporting the physical work test (if applicable)

• installer documentation verifying sourcing compliance and MACR calculations

• the filed tax forms claiming the credit

Working With an Experienced Commercial Solar Installer

Exact Solar has designed and installed solar energy systems for business owners throughout Pennsylvania, New Jersey, and Delaware for more than twenty years. During that time, we’ve seen many national solar companies enter the market and later disappear, leaving customers without long-term support. Our team has always focused on building systems that last and standing behind our work long after installation is complete.

Because we work with commercial solar projects regularly, we also stay closely engaged with evolving federal and state solar policies. Our team dedicates significant time each year to understanding incentive programs, regulatory updates, and utility requirements so we can help our clients navigate the process with confidence.

For businesses considering solar today, that guidance can make an important difference. The federal tax credit is still available, but the timelines and requirements have become more complex.

If your organization is exploring solar for your property, we would be happy to walk through your options and help you understand how the current incentives may apply to your project.

You can schedule a free consultation with our team to review your property, expected system size, and potential eligibility for available solar incentives.